General Guides

General Guides Regional Guides

Regional Guides Starter Guides

Starter Guides

China’s rapidly growing economy and increasing consumer spending power make it an attractive destination for global investors. However, navigating the Chinese market requires a thorough understanding of its unique tax system, which differs significantly from those in Western countries. Compliance with local tax laws is crucial for both local and foreign businesses to operate successfully in China. This article provides a comprehensive overview of the Chinese tax system, highlighting the key taxes and regulations enterprises must be aware of to ensure compliance and optimize their business operations.

Tax System in China

Home to the second-largest economy in the world and a population with continuously increasing spending power, China attracts more global investors each year. While certain accounting practices may remain the same, particular rules in China differ from those in Western countries. Local and foreign businesses operating in China must comply with local laws and regulations, especially regarding taxes. Before the management of an enterprise decides to invest, they should have a comprehensive understanding of the tax system in China and how it works. This article provides a brief overview of the tax system in China.

Which Tax Laws Apply in China?

Several important pieces of legislation govern the tax laws in China. Chinese tax laws have undergone several reforms since their implementation in the early 1980s and continue to evolve. As the economy grows and develops, tax authorities continually aim to promote and create a more stable environment for business. The most relevant tax laws for foreign individuals and companies in China include:

- The Corporate Income Tax (CIT) Law

- The Individual Income Tax (IIT) Law

- The Value Added Tax (VAT) Law

Important Taxes in China

| Tax Type | Standard Rate | Applies To | Notes for Foreign Businesses |

|---|---|---|---|

| Corporate Income Tax (CIT) | 25% | Resident enterprises | Reduced to 15% for encouraged industries |

| Withholding Tax | 10% | Non-resident enterprises | Applies to dividends, royalties, interest |

| Value-Added Tax (VAT) | 13% / 9% / 6% / 3% | Goods & services | Rate depends on industry and taxpayer status |

| Individual Income Tax (IIT) | 3%–45% | Individuals | Residents taxed on worldwide income |

| Consumption Tax | 1%–56% | Specific goods | Luxury and regulated goods |

| Land Appreciation Tax | 30%–60% | Property transactions | Progressive on land value appreciation |

| Stamp Tax | 0.005%–0.1% | Legal documents | Applies to contracts and accounting books |

Operating in China? MSA supports foreign-invested companies with CIT, VAT, and withholding tax compliance to reduce risk and avoid penalties. Message →

Corporate Income Tax

Corporate income tax (CIT) is generally levied against a company’s net income after reasonable business costs and losses are deducted in a financial year. In China, CIT can be settled quarterly or annually, with adjustments refunded or carried forward to the following financial year. The standard CIT rate in China is 25%. However, small and low-profit businesses are entitled to a reduced rate of 20%, and a 15% rate applies to specific encouraged industries, such as high-tech enterprises (see PwC Tax Summaries).

For non-resident enterprises without an establishment in China, the CIT rate is set at 20% on income sourced in China. Certain exemptions or deductions may apply(see China Briefing, Corporate Income Tax in China). Additionally, a concessionary withholding income tax rate of 10% is applicable to interest, rental, royalty, and other passive income for non-residents.

CIT Rates for Small and Low-Profit Businesses:

- Annual profit below RMB 1 million: 2.5%

- Annual profit between RMB 1 million and RMB 3 million: 10%

- Annual profit exceeds RMB 3 million: 25%

All companies in China must submit an Annual Corporate Income Tax Reconciliation Report within five months of their financial year-end to ensure all tax liabilities are met and to determine whether supplementary tax is needed or a tax reimbursement is applicable.

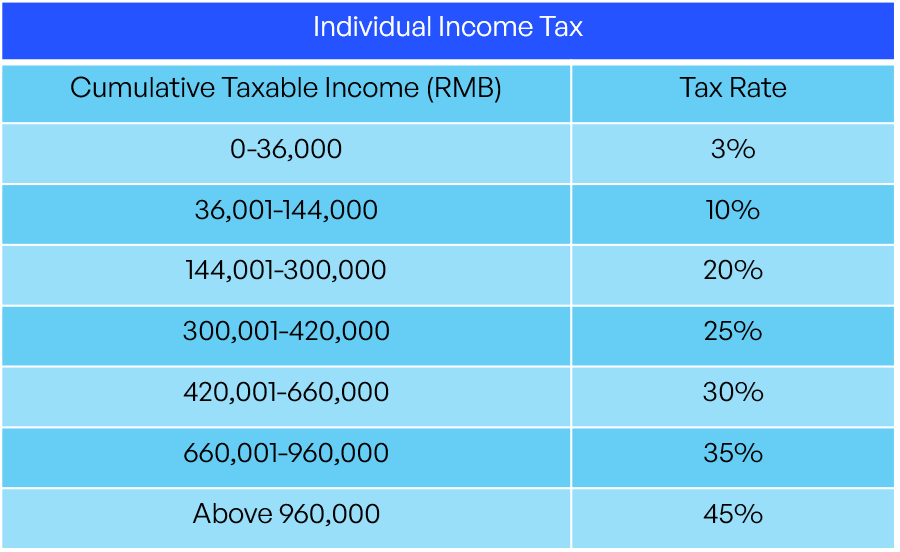

Individual Income Tax

In China, residents are subject to individual income tax on their worldwide income, while non-residents pay tax only on income sourced from China. The individual income tax (IIT) system categorizes income into nine categories. Below is a detailed table summarizing these categories:

| Category | Description | Tax Rate | Additional Information |

|---|---|---|---|

| Employment income | Wages and salaries earned from employment | Progressive rates: 3% to 45% | Includes bonuses, allowances, and other employment-related earnings |

| Income from labor service payment | Payments received for providing labor services | Progressive rates: 3% to 45% | Applies to freelance work, consulting fees, and other service-based income |

| Authors’ remuneration | Income earned from writing and publishing | Progressive rates: 3% to 45% | Includes royalties from books, articles, and other written works |

| Royalty payouts | Payments received for the use of intellectual property | Progressive rates: 3% to 45% | Covers income from patents, trademarks, copyrights, and other intellectual property rights |

| Business/operating income | Income generated from business operations | Progressive rates: 3% to 45% | Applies to income from sole proprietorships, partnerships, and other business activities |

| Rental income | Income earned from leasing property | Progressive rates: 3% to 45% | Includes rental income from residential, commercial, and industrial properties |

| Income from interest, dividends, and bonuses | Income from financial investments, including interest, dividends, and bonus payouts | Progressive rates: 3% to 45% | Covers income from bank deposits, stock dividends, mutual funds, and other financial instruments |

| Income derived from the transfer of property | Gains realized from selling or transferring property | Progressive rates: 3% to 45% | Includes gains from the sale of real estate, stocks, and other personal or business assets |

| Incidental income | Miscellaneous income not covered by other categories | Progressive rates: 3% to 45% | Includes prizes, awards, and other irregular or occasional income |

Comprehensive tax, comprising the first four categories, is taxed on a progressive rate system from 3% to 45%.

Additional Notes

- Residents vs. Non-Residents: Residents are taxed on their worldwide income, while non-residents are taxed only on income sourced from China.

- Progressive Tax Rates: The progressive tax rates for individual income tax in China range from 3% to 45%, depending on the income earned.

- Deductions and Exemptions: Various deductions and exemptions may apply to different income categories, reducing the taxable income amount.

- Tax Filing: Individuals must file their tax returns annually, and in some cases, monthly or quarterly, depending on the nature of their income.

Below, we have tabulated the tax rates applicable to the comprehensive income tax bracket:

Withholding Tax

Withholding tax applies to foreign enterprises operating in China, regardless of whether they have an entity in the country. It is a tax levied on dividends, rents, interest, royalties, and other China-sourced income earned by non-resident enterprises, and is withheld at source before payment is made.

Where income tax applies to Wholly foreign-owned entities and Chinese-foreign joint ventures operating in China, withholding tax applies to income derived in China by non-resident enterprises. For payments made to non-resident enterprises, the tax is withheld before payment is made. The current rate applicable to such enterprises for withholding tax is set at 10%, reduced from the original rate of 20%.

Business Tax

Business tax is no longer applicable in China due to a significant reform of the VAT system (see EY’s commentary on China VAT reform). VAT laws now cover most areas where business tax is relevant and applied.

Business tax is applied to businesses that provide services, transfer intangible properties, and sell and transfer real estate in China. Although it applied to delivering services, it did not apply to processing repair and replacement services). Business tax rates ranged from 3% to 20%.

Value Added Tax (VAT)

One of the most notable changes to the indirect tax system over the past couple of years has been the introduction og a single VAT system for goods and services. VAT applies to the sale of goods, except for those activities which fall under business tax. The VAT rate system in China consists of 3%, 6%, 9%, and 13% rates (see Lorenz-Partners overview of China VAT). The standard VAT rate is 13%, but the applicable VAT rate for general VAT payers depends on the industry.

| Category | Applicable VAT Rate |

|---|---|

| Goods | 13% |

| Services | 6% |

| Small-scale VAT payers | 3% |

| General VAT payers (standard rate) | 13% |

| Lower-tier goods/services (specific items) | 3% |

| Intermediate-tier goods/services (specific items) | 9% |

Other Indirect Taxes in China

Consumption Tax

Consumption tax applies to the importation, selling, manufacturing, and processing of certain goods, such as luxury items. The consumption tax rate varies between 1% and 56%, depending on the class of goods. It applies to 14 categories of consumable goods, including tobacco, alcoholic drinks, cosmetics, jewelry, fireworks, gasoline, diesel oil, tires, motorcycles, automobiles, golf equipment, yachts, luxury watches, disposable chopsticks, and wooden floorboards.

Customs Duties

Customs duties apply to goods that are imported and exported, based on the applicable regulations. Import duties are charged based on the total valuation of the goods.

Stamp Duties

Stamp duties apply to businesses and individuals who receive or execute certain specified documents. The rates vary between 0.005% and 0.1%, depending on the document.

Real Estate Taxes in China

Property taxes apply to owners or users of a building or house and are 1.2% of the original value with deductions or 12% of the rental value. Local governments generally provide tax reductions of between 10% and 30%.

Tax on Resources

Resource taxes apply to natural resources, generally taxed at specific rates set by the Ministry of Finance on a volume or weight basis. Taxable resources include crude oil, natural gas, coal, nonferrous metallic minerals, raw ferrous metals, and raw non-metallic minerals.

Other Specific Taxes

Land Appreciation Tax

A tax levied on gains realized from real property transactions at progressive rates ranging from 30% to 60%. The gain is calculated based on the “land value appreciation amount,” which is the excess of the consideration received from the transfer or sale over the “total deductible amount.”

Vehicle and Vessel Tax

A tax levied at a fixed amount annually on the owners of vehicles and vessels used in China.

Motor Vehicle Acquisition Tax

10% of the taxable consideration is levied on any purchase and importation of cars, motorcycles, trams, trailers, electric buses, carts, and certain types of trucks.

Deed Tax

A tax levied on the transferees or assignees on the purchase, gift, or exchange of ownership of land use rights or real properties, with tax rates generally ranging from 3% to 5%.

Who Regulates Tax Laws in China?

The following bodies are responsible for the introduction, implementation, and amendments of all taxation laws in China:

- The National People’s Congress and its Standing Committee

- The State Council

- The State Administration of Taxation

- The Ministry of Finance

- The State Administration of Foreign Exchange

- The General Administration of Customs

How are Tax Laws Passed in China?

New tax laws in China are promulgated through the following steps:

- Proposal: Relevant government departments establish the proposal and develop an annual work schedule.

- Drafting: Drafts are drawn by the department that establishes the proposal.

- Examination: The legislature examines the draft to ensure it does not conflict with existing laws and meets legislative requirements.

- Publication: The legislature reports their opinions and suggestions to keep writing.

How are Tax Laws Passed in China? (continued)

- Publication: The legislature reports their opinions and suggestions to the Standing Committee of the National People’s Congress. Once the draft is approved, it is published as law.

Key Considerations for Foreign Enterprises

Foreign enterprises (FEs) and foreign investment enterprises (FIEs) must navigate the Chinese tax landscape carefully to ensure compliance and optimize their tax positions. Here are some key considerations:

- Corporate Income Tax (CIT): The standard CIT rate is 25%. However, it can be reduced to 15% for qualified enterprises engaged in industries the Chinese government encourages, such as high-tech enterprises and specific integrated circuits production enterprises. Additionally, various CIT incentives and tax holidays are available for enterprises in encouraged industries.

- Withholding Income Tax: Non-residents receiving passive income such as interest, rentals, and royalties are subject to a withholding tax at a concessionary rate of 10%.

- Individual Income Tax (IIT): IIT rates are progressive, ranging from 3% to 45%, and apply to residents and non-residents on income sourced from China.

- Value-Added Tax (VAT): VAT applies to the sale of goods and the provision of certain services within China. The standard VAT rate is 13%, but certain necessities are taxed at 9%. Small-scale VAT payers are subject to a 3% rate.

- Consumption Tax: This tax applies to 14 categories of consumable goods, including luxury items like tobacco, alcohol, and cosmetics. The tax is computed based on sales price and sales volume.

- Business Tax: This tax applies to the provision of services (excluding processing services and repair and replacement services), the transfer of intangible properties, and the sale of real estate properties. Tax rates range from 3% to 20%.

- Land Appreciation Tax: This tax levies on gains from real property transactions at progressive rates ranging from 30% to 60%.

- Resource Tax: Levied on natural resources, this tax is generally based on tonnage or volume at rates specified by the Ministry of Finance.

- Real Estate Tax: This tax is imposed on the owners, users, or custodians of houses and buildings at either 1.2% of the original value with certain deductions or 12% of the rental value.

- Vehicle and Vessel Tax: A fixed amount is levied annually on the owners of vehicles and vessels used in China.

- Motor Vehicle Acquisition Tax: A 10% tax is levied on the purchase and importation of cars, motorcycles, trams, trailers, electric buses, carts, and certain types of trucks.

- Stamp Tax: This tax is levied on enterprises or individuals who execute or receive specified documentation in China, with rates varying between 0.005% and 0.1%.

- Customs Duties: Duties are imposed on goods imported into China and are generally assessed on the CIF (cost, insurance, and freight) value. The duty rate depends on the imported goods’ nature and country of origin.

- Deed Tax: This tax is levied on the transferees or assignees on the purchase, gift, or exchange of ownership of land use rights or real properties, with tax rates generally ranging from 3% to 5%.

Schedule a complimentary tax health-check with MSA and receive a tailored action plan to minimise risk and maximise incentives Message →

China’s tax system is multi-layered, combining corporate income tax, value-added tax, individual income tax, and dozens of regional surcharges and special incentives—making effective tax planning both critical and complex. Recent reforms have tightened compliance monitoring and closed loopholes, yet legitimate tax optimization opportunities remain for companies with proper structuring. MSA Asia helps you understand your obligations under China tax filing requirements. Drop us a line to audit your current structure.